Depository Function and Framework

Depositories enable investors to open and manage demat accounts through registered Depository Participants (DPs). It plays a critical role in the Indian capital markets by providing services such as dematerialization, rematerialization, settlement of trades, corporate action processing, e-voting, and KYC verification.

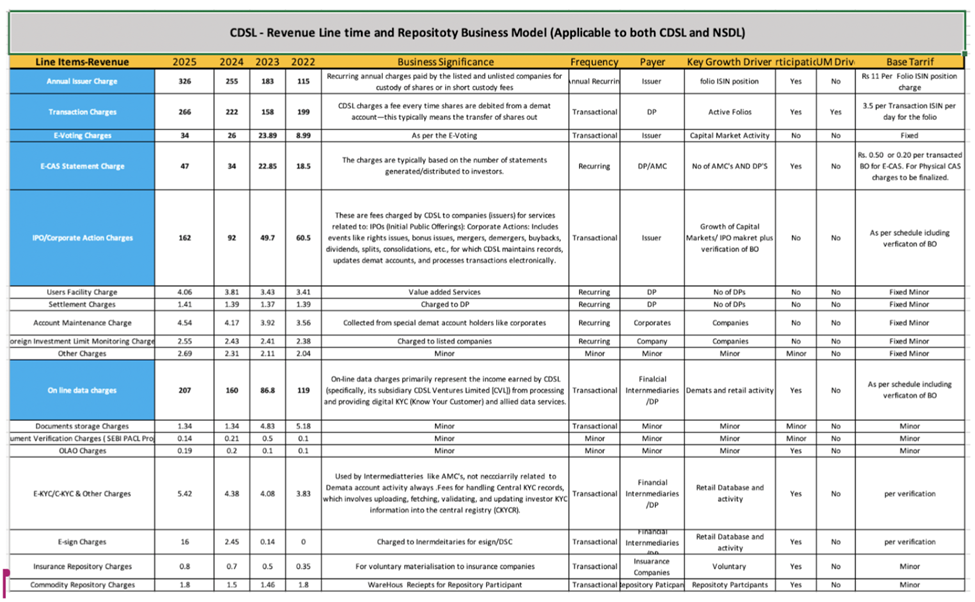

CDSL Revenue Structure and Key Contributors

Central Depository Services (India) Limited (CDSL) earns revenue through a range of charges levied on issuers, intermediaries, and investors. Around 90% of its revenue is driven by four key streams: Annual Issuer Charges (30%), which are recurring fees paid by listed and unlisted companies for custody of securities; Transaction Charges (25%), levied each time securities are debited from a demat account; Online Data Charges (19%), earned primarily through CDSL Ventures Limited (CVL) for digital KYC and allied services; IPO/Corporate Action Charges (15%), collected for handling IPOs and corporate actions such as rights issues, mergers, and dividends. Other Service Charges(10%), which include fees from services like e-voting, e-CAS statements, account maintenance, e-KYC/C-KYC processing, document verification, and commodity repository functions.

Revenue from AUM vs Revenue from Demat account

Annual Issuer Charges

These are fixed annual fees charged to listed and unlisted companies for the custody of their securities. The charges are based on folio-level ISIN positions and are directly driven by the number of demat accounts held by retail investors. This revenue stream is entirely retail participation-driven and not influenced by AUM.

Transaction Charges

These charges are incurred whenever securities are debited from a demat account, typically during sell-side transactions. They are levied per ISIN on a daily basis. The growth in this segment is supported by both an increase in active demat accounts (retail participation) and the overall value of holdings (AUM), making it a mix of both volume and asset-driven factors.

IPO/Corporate Action Charges

These fees are paid by issuers for services related to IPOs and various corporate actions such as rights issues, bonus shares, mergers, and buybacks. This revenue is not influenced by the number of demat accounts or AUM. Instead, it is closely tied to the activity level in the primary capital markets — particularly the frequency and scale of IPOs and the need for Beneficial Owner (BO) verification.

Online Data Charges

This revenue arises from digital services such as KYC processing and data handling provided by CDSL Ventures Ltd. The charges are transactional and scale with the volume of investor onboarding and updates. The growth of this segment is entirely dependent on the number of demat accounts and retail activity, with no link to AUM.

Other Charges (E-voting, E-CAS, Maintenance, KYC, etc.)

Most of the remaining revenue heads — including e-voting, statement charges, maintenance fees, KYC services, and others — are fixed or minor in nature and largely independent of AUM.

In conclusion, more than 75% of CDSL’s revenue comes from retail participation and the number of demat accounts, not from the value of assets held.

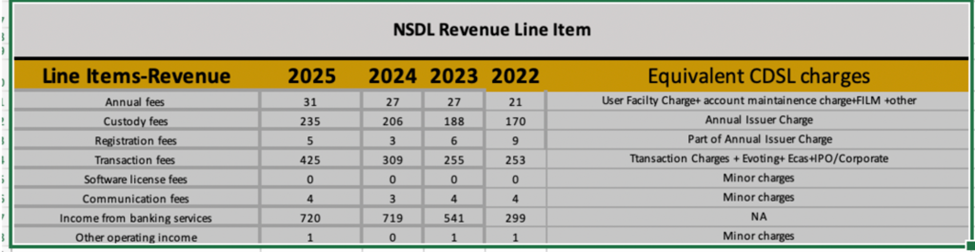

NSDL Revenue Structure and Key Contributors

In NSDL’s revenue structure, transaction fees contribute 30%, which likely includes components that CDSL reports separately — such as transaction charges, e-voting, e-CAS, and IPO/corporate action charges. Custody fees account for 17%, which corresponds to CDSL’s annual issuer charges, representing revenue from securities held in custody. Additionally, 51% of NSDL’s revenue comes from its subsidiary that provides banking-related services. While not part of its core depository operations, it forms a major portion of the overall revenue mix.

Revenue from AUM vs Revenue from Demat account

Custody fees are analogous to the Annual Issuer Charges levied by CDSL. These charges are independent of the Assets Under Management (AUM) and are primarily driven by the number of retail participants. They are annual recurring charges paid by the issuer.

Transaction Fees

Transaction fees are a combination of various revenue components such as Transaction Charges, e-Voting, e-CAS, and IPO/Corporate action-related charges, similar to the structure followed by CDSL. Some of these charges are independent of the Assets Under Management (AUM), while others are influenced by the number of retail participants and demat accounts.

Other Service Fees

The revenue structure also includes several other components such as Annual Fees, Registration Fees. Additionally, there are minor contributions from charges like Software License Fees, Communication Fees, and Other Operating Income. Income from banking services, though not part of core depository operations, constitutes a substantial share of overall revenue.

Comparison of Demat Value of CDSL vs Demat Value of NSDL

In FY2025, the total demat value held with NSDL stood at ₹464 trillion, significantly higher than CDSL’s ₹70.5 trillion. Back in FY2022, NSDL’s demat value was ₹301.8 trillion, while CDSL’s was ₹37.17 trillion. Over this three-year period, NSDL recorded a compound annual growth rate (CAGR) of approximately 15.3%, whereas CDSL exhibited a faster growth trajectory with a CAGR of 23.5%. This indicates that while NSDL continues to dominate in absolute terms, CDSL has been expanding at a significantly higher pace.

Comparison of Demat accounts of CDSL vs Demat accounts of NSDL

NSDL and CDSL serve distinct segments of India’s depository ecosystem, each holding a leadership position in their respective domains. NSDL continues to maintain a stronghold among institutional and high-value clients, managing over 4.04 crore active client accounts, including more than 4 lakh accounts linked to debt instruments. On the other hand, CDSL has emerged as the preferred platform for retail investors, with over 15.86 crore investor accounts as of June 30, 2025—nearly four times that of NSDL. This stark contrast highlights NSDL’s institutional dominance, while CDSL commands a significantly broader retail reach.

Conclusion

Based on the overall assessment, the contribution of charges linked to demat accounts appears to be higher compared to charges related to AUM, backed by charges like Annual Issuer Charges, Online Data Charges, etc. Depositories are regulated by SEBI hence have similar tariff structure to great extent. This compels to conclude – market share in Demat accounts is the key driver of growth.