This is third and conclusive part of our series : Make Wealth from Health. We had concluded in last article that base line ARPOB growth is 8% and hospitals will be able to maintain margins as they have demonstrated pricing power in last decade.

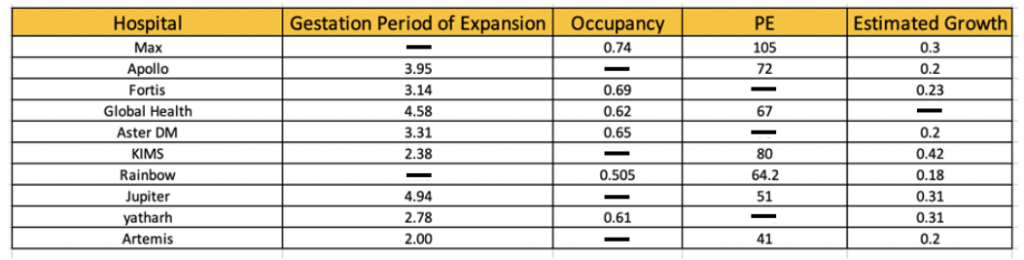

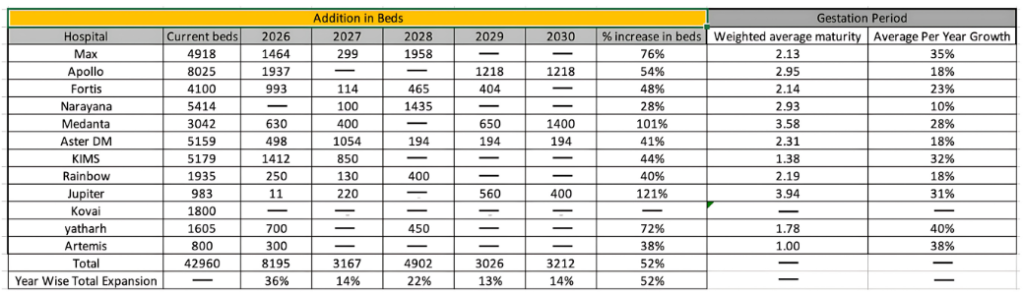

The growth above 8% will be driven by capacity Expansion. Here is detailed table covering major hospitals:

The next step to analysis is making a STRENGTH model , how efficiently and likely will hospitals cashify this capex plan. The metrics which may influence this:

1) Estimated ARPOB Growth

2) Gestation Period of Capex

3) Per Year Growth as per gestation period

4) Target Geography of Expansion (Metro and Non Metro) – We have seen that ARPOB is much lower and capacity utilization is much slower in new geography or a non metro geography

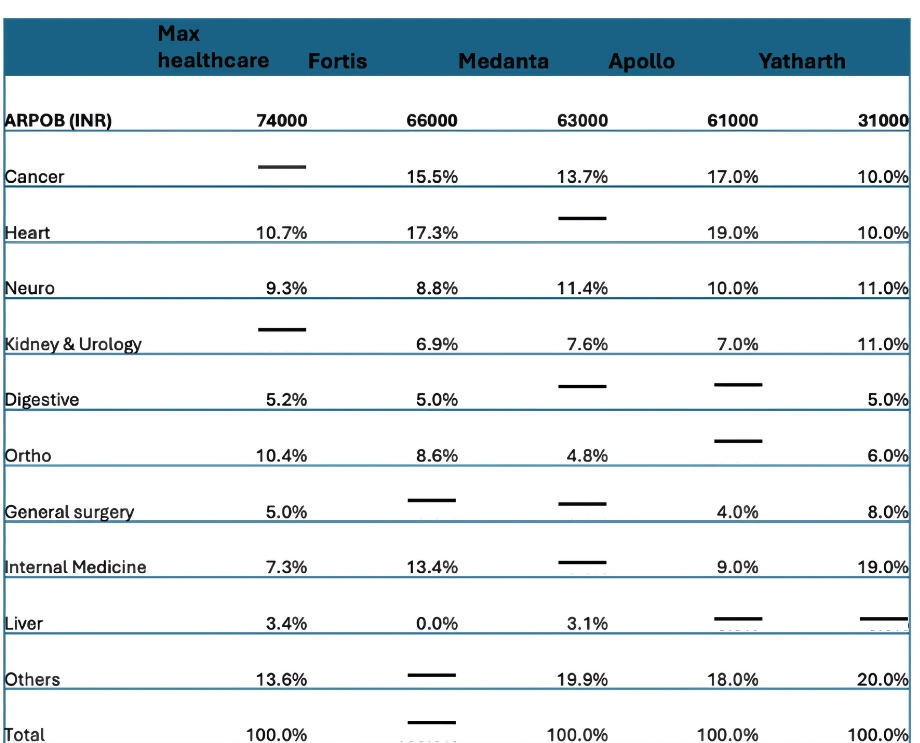

5) Specialty Mix- A greater specialty mix enables for higher ARPOB

6) Brand Equity -Market positioning enables the steeper growth in occupancy

7) Doctor Retention and Management are qualitative enablers

Below is strength model which can be used to deliberate on decision making

Specialty mix better for ARPOB

A hospital’s specialty mix directly influences its ARPOB, and thereby its revenue performance. Among the compared hospitals, Max Healthcare leads with the highest ARPOB of 74,000, followed by Fortis (*66,000) and Medanta (*63,000). These hospitals allocate a significant proportion of their services to high-revenue specialties such as oncology, cardiology, neurology, and orthopaedics-together forming over 60% of their case mix. For instance, Max derives 25.8% of its revenue from cancer treatment alone, a complex and high-margin segment. In contrast, Yatharth, with an ARPOB of *31,000, has a relatively lower focus on such high-value specialties and a larger share in low-ARPOB segments like internal medicine and general surgery. This correlation clearly indicates that hospitals with a greater focus on specialized care not only attract higher-paying procedures but also achieve stronger unit economics through superior ARPOB, thereby enhancing overall revenue performance.

Conclusion: The hospital industry is poised for yet another growth in mid term 5 to 7 years. On the quantitative side in mid term , the smaller the gestation period and metro concentration coupled with brand equity will give higher and certain growth.

On the qualitative remark, the long term growth will be driven by penetration of medical insurance as metro cities saturate. Hospitals which can recruit and retain doctors and make healthcare affordable and inclusive will create wealth for investors.

For Reference -Quick Analysis