Imagine reaching retirement—decades of hard work behind you. Now, you don’t want to worry about money every month. You want a peaceful, predictable income. That’s exactly what annuity plans promise.

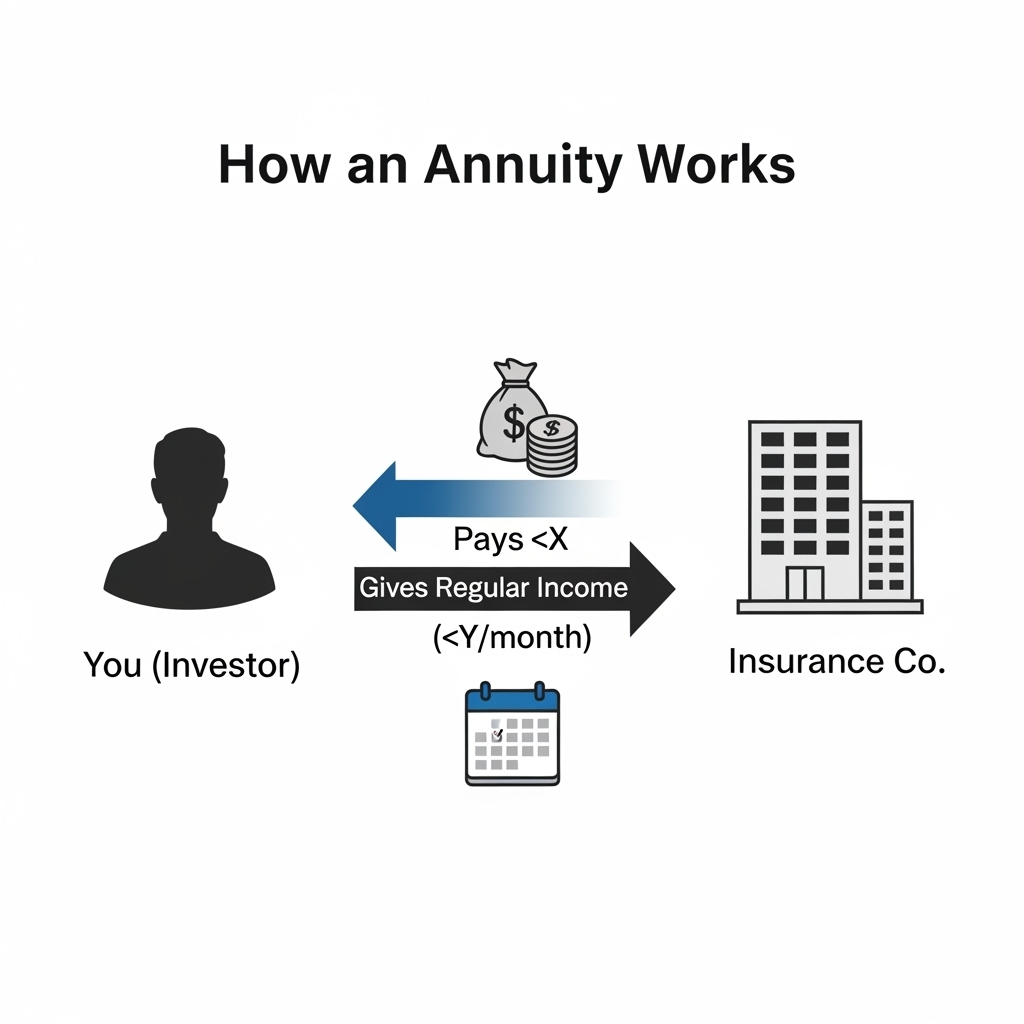

An annuity plan is a retirement-focused financial instrument that ensures a regular flow of income. You can invest either a lump sum amount or contribute periodically to an insurance company. In return, the insurer commits to paying you a fixed income at regular intervals—monthly, quarterly, or annually—either for a specified duration or for the remainder of your life..

In other words, annuities convert your savings into a predictable pension—a concept that has gained popularity especially in times of rising longevity and uncertain market returns.

But here’s the real question:

Are annuity plans truly solving the retirement problem—or are they just a well-marketed product with more drawbacks than benefits?

By the end of this post, you’ll have a clear, no-fluff understanding of annuities—and whether they’re the right fit for your financial journey.

How Do Annuity Plans Work?

Let’s break this down in the simplest way possible.

An annuity is more than just a financial product—it’s a formal agreement between you and an insurance company. Under this arrangement, you contribute either a one-time lump sum or make periodic payments. In exchange, the insurer promises to provide you with a fixed, regular income either for a set number of years or for the rest of your life.

Sounds simple? It is. But let’s explore what really happens behind the scenes.

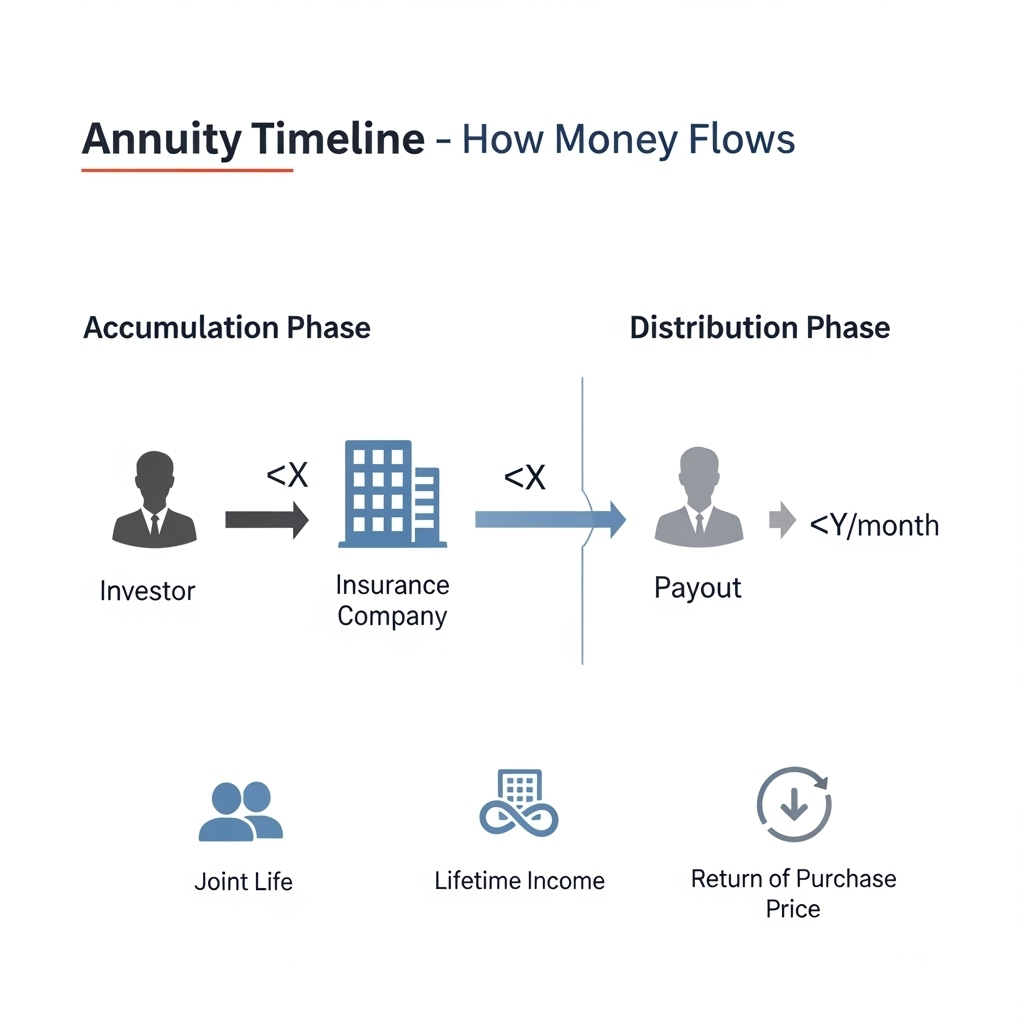

Two Phases of an Annuity Plan

Annuities typically go through two main phases:

1. Accumulation Phase

This is the period when you’re still investing. You can either:

– Pay a lump sum (say ₹10 lakhs at once), or

– Contribute periodically (monthly or yearly premiums over, say, 10 years).

During this phase, the money is either:

– Locked at a fixed interest rate (in case of fixed annuities), or

– Invested in market-linked instruments (in case of variable annuities).

This phase is optional in immediate annuities, which skip straight to payouts.

2. Distribution Phase

Once the annuity “matures” (or if you choose an immediate plan), the insurer starts paying you back. This can happen:

Monthly

Quarterly

Half-yearly

Annually

…and continues until the end of the term or your lifetime—depending on the plan you choose.

Your Annuity = Your Contribution + Returns – Charges

It’s important to understand: annuities are not magic income generators. The insurer is simply:

= Investing your money safely,

– Locking in an interest rate or using market products (in some cases), and

– Giving you part of the principal plus interest back, while deducting their charges.

You’re essentially turning a pool of money into a paycheck.

Immediate vs Deferred Annuities: Key Difference

| Type | When Payouts Start | Ideal For |

|---|---|---|

| Immediate | Right after you invest | Retirees seeking income now |

| Deferred | After a few years | Young professionals planning for future retirement |

In India, immediate annuities are common for retirees using NPS corpus or EPF savings. Deferred annuities are useful if you’re still working and want income to start post-retirement.

Types of Annuities

Not all annuity plans are created equal. Some offer guaranteed returns, while others offer higher potential—but with risks. Choosing the right one depends entirely on your goals, risk tolerance, and how soon you need income.

Let’s explore the major types:

1. Fixed Annuity

This is the most basic and popular option in India.

– You receive a fixed amount of money at regular intervals—monthly, quarterly, etc.

– The insurer declares an interest rate (say, 6% annually) at the start.

– Ideal for retirees looking for stable, predictable income.

Common in India through plans like LIC Jeevan Akshay, HDFC Life Immediate Annuity Plan etc

🟢 Pros: No market risk, easy to understand

🔴 Cons: Returns often lower than inflation

2. Variable Annuity (More common in the U.S.)

– Your annuity is linked to mutual fund-like investments.

– Payments vary depending on market performance.

– Best for those comfortable with some volatility in returns.

Note: Variable annuities are less popular in India due to regulatory concerns and investor conservatism.

🟢 Pros: Higher upside potential

🔴 Cons: Risky in volatile markets, complex to manage

3. Indexed Annuity

– Tied to a market index like Nifty 50 or S&P 500.

– Your returns depend on index performance, but with a guaranteed minimum.

Example use-case: A 50-year-old wants exposure to markets but can’t afford to lose principal

🟢 Pros: Some market-linked growth + downside protection

🔴 Cons: Return caps; gains are limited

4. Life Annuity / Joint Life Annuity

– Life Annuity: You receive income for your lifetime.

– Joint Life Annuity: Continues to your spouse after your death.

Example Plans: ICICI Pru Immediate Annuity , Kotak Lifetime Income Plan

🟢 Pros: Lifetime protection for your family

🔴 Cons: Lower monthly payout than single-life options

5. Annuity with Return of Purchase Price (ROP)

– You receive regular income during your life.

– After death, your initial investment is returned to nominee.\

This is a popular option among conservative investors in India, especially NPS subscribers.

🟢 Pros: Income + capital safety

🔴 Cons: Payouts are usually lower than plans without ROP

6. Term-Certain Annuity

– Pays for a fixed period (e.g., 10 or 20 years), regardless of whether you’re alive.

– Ideal if you want to guarantee income for dependents even after death.

🟢 Pros: Useful for estate planning

🔴 Cons: May not be suitable if you outlive the term

Annuity Plans vs Other Retirement Options (with Market Comparison)

Now that you understand what annuities are and the types available, the natural question is:

Let’s break this down in terms of features that matter to real investors: returns, flexibility, tax, and risk.

The annuity rate you receive will vary based on the specific annuity option you choose.

The amount of monthly pension you receive depends on the type of annuity plan you choose. The portion of your NPS retirement savings used to purchase the annuity is referred to as the “purchase price.” Some annuity options include a feature where the purchase price is returned to the nominee after the death of the annuitant—this is called an annuity with Return of Purchase (ROP). In contrast, annuities without ROP do not return the invested amount after death. These non-ROP plans generally offer higher monthly payouts compared to ROP options.

Life Annuity Without Return of Purchase (ROP)

In the life annuity option under NPS, the subscriber receives a fixed monthly income for as long as they live. If the plan does not include the Return of Purchase (ROP) feature, the payments stop entirely upon the death of the annuitant, and no further amount is given to any nominee. On the other hand, if the plan includes ROP, the original investment amount is returned to the nominee after the annuitant’s death.

Life Annuity: Monthly Income on ₹1 Crore Investment

As mentioned earlier, annuity rates and payouts vary depending on the insurer offering the plan. The range can be significant — with the highest rate at 7.05% and the lowest at 5.64%. For someone investing ₹1 crore in a life annuity plan, the monthly payout difference between the highest and lowest provider comes to ₹11,733. Over a 30-year retirement period, this gap could lead to a total shortfall of approximately ₹42.24 lakh. For an investment of ₹50 lakh, the difference in returns could amount to around ₹21.12 lakh over the same duration.

| Purchase price to be returned to nominee | Yes | Yes | No | No |

| Annuity service provider | Monthly Amount | Rate (Annual) | Monthly Amount | Rate (Annual) |

| Shriram Life Insurance Co Ltd | 58763 | 7.05% | 77432 | 9.29% |

| MAX Life Insurance Co Ltd | 58872 | 7.06% | 75536 | 9.06% |

| Bajaj Allianz Life Insurance Co Ltd | 58518 | 7.02% | 64407 | 7.73% |

| ICICI Prudential Life Insurance Co Ltd | 58309 | 7.00% | 61997 | 7.44% |

| IndiaFirst Life Insurance Co Ltd | 59058 | 7.09% | 72641 | 8.72% |

| TATA AIA Insurance Co Ltd | 58204 | 6.98% | 63105 | 7.57% |

| Aditya Birla Sun Life Insurance Co Ltd | 57432 | 6.89% | 70969 | 8.52% |

| HDFC Life Insurance Co Ltd | 56239 | 6.75% | 74396 | 8.93% |

| Life Insurance Corporation of India | 56160 | 6.74% | 75473 | 9.06% |

| Kotak Mahindra Life Insurance Co Ltd | 54714 | 6.57% | 68804 | 8.26% |

| Canara HSBC Life Insurance Co Ltd | 54854 | 6.58% | 67516 | 8.10% |

| SBI Life Insurance Co Ltd | 53779 | 6.45% | 65244 | 7.83% |

| Star Union Dai-ichi Life Insurance Co Ltd | 52729 | 6.33% | 71388 | 8.57% |

| PNB Metlife India Insurance Co Ltd | 51652 | 6.20% | 63258 | 7.59% |

| Edelweiss Tokio Life Insurance Co Ltd | 48176 | 5.78% | 63894 | 7.67% |

Source: CRA-NSDL, annuity rates as on 26 September 2024 for annuitant of age 60 years, spouse of age 55 years

Joint Life Annuity Without Return of Purchase (ROP)

In the joint life annuity option under NPS, the subscriber receives a fixed monthly payout for life. After their death, the same amount continues to be paid to the spouse. If the plan is without the Return of Purchase (ROP) feature, the payments stop entirely once both the subscriber and spouse pass away, and no further benefits are provided. However, if the plan includes the ROP option, the original purchase amount is returned to the nominee after the death of both annuitants.

Joint life annuity – Monthly annuity income on Rs 1 crore investment

| Purchase price to be returned to nominee | Yes | Yes | No | No |

| Annuity service provider | Monthly Amount | Rate (Annual) | Monthly Amount | Rate (Annual) |

| Shriram Life Insurance Co Ltd | 58719 | 7.05% | 67252 | 8.07% |

| MAX Life Insurance Co Ltd | 58672 | 7.04% | 65168 | 7.82% |

| Bajaj Allianz Life Insurance Co Ltd | 58308 | 7.00% | 54184 | 6.50% |

| ICICI Prudential Life Insurance Co Ltd | 58215 | 6.99% | 54222 | 6.51% |

| IndiaFirst Life Insurance Co Ltd | 58138 | 6.98% | 58883 | 7.07% |

| TATA AIA Insurance Co Ltd | 57796 | 6.94% | 55243 | 6.63% |

| Aditya Birla Sun Life Insurance Co Ltd | 57683 | 6.92% | 61611 | 7.39% |

| HDFC Life Insurance Co Ltd | 55998 | 6.72% | 64916 | 7.79% |

| Life Insurance Corporation of India | 55903 | 6.71% | 64743 | 7.77% |

| Kotak Mahindra Life Insurance Co Ltd | 54054 | 6.49% | 59410 | 7.13% |

| Canara HSBC Life Insurance Co Ltd | 53692 | 6.44% | NA | NA |

| SBI Life Insurance Co Ltd | 53505 | 6.42% | 57806 | 6.94% |

| Star Union Dai-ichi Life Insurance Co Ltd | 52146 | 6.26% | 60742 | 7.29% |

| PNB Metlife India Insurance Co Ltd | 51529 | 6.18% | 57350 | 6.88% |

| Edelweiss Tokio Life Insurance Co Ltd | 46986 | 5.64% | 54293 | 6.52% |

NPS Family Pension – With Return of Purchase (ROP)

In the joint life annuity option under NPS, the subscriber receives a monthly pension for life. After their death, the same pension amount continues to be paid to the spouse. If the spouse also passes away, the pension is then passed on to the dependent mother, followed by the dependent father, if applicable. Once all listed beneficiaries (annuitants) have passed away, the annuity payments stop, and the entire purchase amount is returned to the subscriber’s children or legal heirs. This particular annuity plan under NPS is available only with the Return of Purchase (ROP) option, ensuring that the invested corpus is given back to the nominee after the demise of all covered individuals.

NPS – family income with ROP – Monthly annuity on Rs 1 crore investment

| Annuity Service Provider | Monthly Amount | Rate (Annual) |

| Shriram Life Insurance Co Ltd | 58719 | 7.05% |

| MAX Life Insurance Co Ltd | 58672 | 7.04% |

| Bajaj Allianz Life Insurance Co Ltd | 50900 | 6.11% |

| ICICI Prudential Life Insurance Co Ltd | 49530 | 5.94% |

| IndiaFirst Life Insurance Co Ltd | 58138 | 6.98% |

| Aditya Birla Sun Life Insurance Co Ltd | 57683 | 6.92% |

| HDFC Life Insurance Co Ltd | 55998 | 6.72% |

| Life Insurance Corporation of India | 55903 | 6.71% |

| Kotak Mahindra Life Insurance Co Ltd | 54714 | 6.57% |

| Canara HSBC Life Insurance Co Ltd | 51470 | 6.18% |

| SBI Life Insurance Co Ltd | 53505 | 6.42% |

| Star Union Dai-ichi Life Insurance Co Ltd | 52146 | 6.26% |

| PNB Metlife India Insurance Co Ltd | 51529 | 6.18% |

| Edelweiss Tokio Life Insurance Co Ltd | 46986 | 5.64% |

How Competitive Are Annuity Rates in India?

At first glance, annuity returns might seem less attractive compared to several other secure fixed-income options currently available. For example, schemes like the Post Office Senior Citizens Savings Scheme offer an interest rate of 8.2%, RBI’s Floating Rate Savings Bonds yield 8.05%, SBI’s “We Care” fixed deposit provides 7.5%, and even the Post Office Monthly Income Scheme (MIS) delivers 7.4%. Additionally, many senior citizen FDs across banks are offering close to 8%. However, it’s important to note that these higher returns are typically fixed only for a limited term—usually between 5 to 10 years. There’s no certainty that the same rates will be available when these instruments mature and are renewed. On the other hand, annuity payouts, though generally lower, are locked in for life, shielding the investor from future interest rate fluctuations.

Are Annuities Really Solving the Retirement Problem?

Annuities promise peace of mind. But in a world where inflation never sleeps and life expectancy keeps rising, do they actually deliver?

Let’s analyze this question from three angles:

1. The Problem Annuities Claim to Solve: Longevity Risk

Longevity risk is the risk of outliving your savings. Imagine living till 90 or 95, but your investments run dry by 80. Scary, right?

This is where annuities shine:

They guarantee income for life (in life annuity options)

They remove the stress of “will my money last?”

So in theory, they do solve a major retirement problem.

But the real issue isn’t just about how long you live—it’s also about how much your money is worth while you live.

2. But Do They Beat Inflation?

Most annuities in India offer 5.5%–6.5% returns. Inflation, especially for healthcare and essentials, averages 6%–7%, and sometimes more.

Example:

If you invest ₹20 lakhs and get ₹11,000/month, it may feel enough today.

But after 15 years?

That ₹11,000 could feel like ₹6,000 in today’s terms due to inflation erosion.

Unless you’re choosing inflation-adjusted annuities (which often offer lower starting payouts), you’re losing real purchasing power every year.

3. Tax Efficiency: A Silent Killer

Unlike debt funds or PPF, annuity payouts are fully taxable as income.

This can push senior citizens into higher tax brackets and reduce net income by 10–30% depending on slab.

So… Are They Worth It?

YES, annuities solve one major problem — lifetime income.

But NO, they don’t fully solve the retirement challenge unless:

– You combine them with inflation-beating assets like equity mutual funds or REITs.

– You are not relying on them as your only retirement income source.

📢 Think of annuities as a “safety net,” not the whole mattress.

For whom are annuities ideal?

– Retirees without family support

– People who can’t manage market investments themselves

– Those who prefer predictable income over chasing high returns

Final Verdict – Are Annuities Attractive or Overrated?

Annuities are one of the most debated retirement products out there.

Some financial planners call them “boring but safe.” Others say they’re “overhyped insurance traps.”

So what’s the truth?

Let’s distill everything we’ve explored into a clear decision framework:

✅ When Annuities are Attractive

✔️ You want peace of mind with predictable monthly income

✔️ You’re risk-averse and dislike market volatility

✔️ You’ve already covered other financial goals like emergencies, health insurance, etc.

✔️ You’re nearing retirement (60+) and don’t want to actively manage investments

✔️ You need to bridge pension gaps after exhausting NPS/EPF

In these cases, annuities act like a personal pension plan — slow, steady, and stress-free.

❌ When Annuities Might Be Overrated

✖️ You expect your money to grow and beat inflation over 15–20 years

✖️ You’re comfortable managing mutual funds or passive index investing

✖️ You want tax-efficient income (annuities are taxed at slab rate)

✖️ You’re still in your 40s or early 50s — you have time on your side

In such scenarios, a mix of equity mutual funds, debt funds, and REITs may offer better flexibility, returns, and liquidity.

🧾 Quick Summary Table:

| Criteria | Annuity Score |

|---|---|

| Safety | ★★★★★ (High) |

| Return Potential | ★★☆☆☆ (Low) |

| Inflation Protection | ★★☆☆☆ (Weak) |

| Tax Efficiency | ★★☆☆☆ (Poor) |

| Simplicity | ★★★★☆ (Good) |

| Liquidity | ★☆☆☆☆ (Very Low) |